Today, the conveyor belt market in mining faces unprecedented pressure and opportunity. The global push for electrification and renewable energy has triggered explosive demand for lithium, copper, cobalt, and rare earth elements. According to the International Energy Agency, lithium demand surged nearly 30% in both 2023 and 2024, forcing mining operations to scale faster than ever. That scale-up demands conveyor systems capable of moving more material, over longer distances, with less downtime.

This article examines the current market size and growth projections, the economic and regulatory drivers reshaping demand, how the market segments by belt type and application, which regions lead growth, and the technology shifts—from IoT sensors to gearless drives—that are redefining what mining operators expect from their conveyor systems.

TLDR: Key Takeaways at a Glance

- Mining conveyor belt market estimated at ~$3 billion in 2024, projected to surpass $4–$7 billion by 2033 at 3.75–6.1% CAGR

- Critical minerals boom (lithium, copper, cobalt) and automation adoption are primary demand drivers

- Steel cord belts dominate heavy-duty applications (47% share); textile and aramid belts serve lighter-duty and underground roles

- Asia-Pacific leads the market; Latin America represents fastest growth due to copper and lithium extraction

- IoT-enabled predictive maintenance is reshaping conveyor lifecycle economics and reducing unplanned downtime

Market Size and Growth Projections

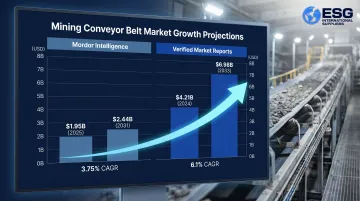

The global conveyor belt market serving mining operations is valued between $1.95 billion and $4.21 billion in 2024 — a wide range that reflects whether the analysis covers raw belting only or includes system components and aftermarket services.

Verified Market Reports puts the figure at $4.21 billion in 2024, forecasting growth to $6.98 billion by 2033 at a 6.1% CAGR. Mordor Intelligence is more conservative, estimating $1.95 billion in 2025 and $2.44 billion by 2031 at a 3.75% CAGR.

A CAGR of 4–6% signals sustained capital investment in material handling infrastructure — not one-time replacement purchases. It reflects genuine confidence that mineral extraction volumes will rise and that aging truck-based haulage systems will keep transitioning to belt-based transport as mines expand geographically.

Regional Focus: North America

The U.S. mining conveyor belt market is a mature, substantial segment within the global picture. Widely circulated figures of $4.21 billion to $6.98 billion represent the global market — the U.S. accounts for a meaningful but smaller share, driven by copper and precious metals operations in Nevada and Arizona, plus coal extraction in Appalachia.

These regional dynamics connect to broader demand forces shaping the global outlook:

- Rising global mineral demand tied to EV and clean energy infrastructure

- Infrastructure investment in mining-heavy regions (Chile, Peru, Australia, China)

- Transition from truck haulage to belt transport in expanding open-pit and new underground mines

- Federal and state incentives for domestic critical mineral production in North America

Uncertainty factors:

Commodity price swings remain the primary wildcard. When copper or lithium prices drop sharply, mining companies freeze capex — and belt infrastructure budgets are among the first cuts. Geopolitical risk in key producing regions and shifting lithium supply-demand dynamics also cause research firms to model different scenarios, which explains the wide gap between published valuations.

Key Market Drivers and Restraints

What Is Driving Demand?

Critical Minerals Boom

The energy transition has fundamentally reshaped mining demand. Lithium demand rose nearly 30% in both 2023 and 2024, while nickel, cobalt, graphite, and rare earths grew 6–8% annually. Mines extracting these materials require high-capacity, continuous belt systems to remain cost-competitive. Conveyor belts enable 24/7 throughput that truck fleets cannot match at scale.

Economics of Belt vs. Truck Haulage

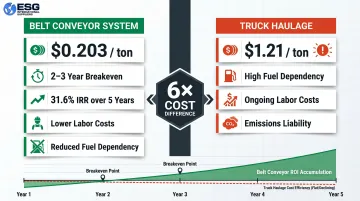

BEUMER Group's economic modeling shows conveying costs at $0.203 per ton versus $1.21 per ton for truck haulage. For a 5-mile transport route moving 5 million tons annually, the capital investment in an In-Pit Crushing and Conveying (IPCC) system breaks even in 2–3 years, delivering a 31.6% internal rate of return over five years. These savings stem from reduced labor, fuel costs, and maintenance requirements.

Energy Efficiency and Sustainability Compliance

Research shows belt conveyors consume 4 to 12 times less energy than truck haulage, with CO2 emissions 3 to 10 times lower. As mining companies face stricter environmental, social, and governance (ESG) mandates from investors and regulators, the case for conveyor systems strengthens.

Open Pit to Underground Transition

Many major open-pit mines are reaching their depth limits, forcing operations underground. This shift increases demand for specialized conveyor systems designed for confined spaces, steep inclines, fire-risk environments, and ventilation constraints.

Underground belts must meet higher standards for fire resistance, emissions control, and sensor-enabled condition monitoring — requirements that drive active replacement and upgrade cycles across mature operations.

Regulatory Compliance

Stricter safety and environmental regulations compel mining operators to retire legacy conveyor systems. Newer models meet updated fire-resistance standards, dust-control requirements, and safety certifications—creating a replacement demand layer on top of new installation demand.

What Is Restraining Growth?

Strong demand fundamentals don't eliminate structural barriers. Two factors consistently slow market penetration:

- High upfront capital: Belt procurement, installation, idler frames, drive systems, and structural support represent a significant investment. Smaller operators or mines navigating uncertain commodity prices often delay adoption as a result.

- Retrofitting complexity: Mines built around truck haulage must redesign pit layouts, relocate crushers, and reconfigure material flow — all while keeping production running. The engineering and logistical burden is steepest at mature operations already locked into existing infrastructure.

Market Segmentation: Types, Applications, and What They Mean for Buyers

By Belt Type: Steel Cord vs. Textile Reinforced

Steel Cord Belts dominate the market with a 47.17% share in 2025. These belts offer superior tensile strength (630 N/mm to 5,400+ N/mm) and minimal elongation (~0.2%), making them ideal for:

- Long-distance overland transport (5+ miles)

- High vertical lifts (1,000+ meters underground)

- Heavy bulk material (iron ore, coal, copper concentrate)

Textile-Reinforced (Fabric) Belts use polyester/nylon (EP) or nylon/nylon (NN) plies. They're lighter, more flexible, and cost-effective for:

- Shorter transport runs (<500 meters)

- Surface mining applications with moderate loads

- High-impact loading zones where flexibility absorbs shock

Specialty Materials: Aramid and hybrid belts represent a smaller but fast-growing niche, advancing at 4.22% CAGR. These lightweight, high-strength belts suit underground declines and curved overland routes, reducing energy consumption while maintaining breaking strength.

Each belt type maps to a specific operating profile:

- Steel cord: Long hauls, deep underground, high tonnage

- Textile: Short hauls, surface operations, flexibility priority

- Aramid/hybrid: Underground confined spaces, energy efficiency focus

By Application: Coal, Precious Metals, and Beyond

Belt type selection doesn't happen in isolation — the application environment determines which specifications actually matter in the field.

Coal mining remains the largest application segment due to massive bulk material volumes. However, the gold, silver, and base metals segment (copper, lithium, iron ore) is growing fastest, aligned with the critical minerals boom.

| Application | Conveyor Priorities |

|---|---|

| Surface Mining | High-capacity overland systems, long single-flight runs (5–15 miles), resistance to UV and weather |

| Underground Mining | Fire-resistant covers, dust control, confined-space installation, steep inclines, ventilation compatibility |

Buyers must specify application environment carefully — underground belts require certifications (flame resistance, low smoke emission) that surface belts don't.

Regional Breakdown: Where Growth Is Concentrated

Asia-Pacific Leads, But Americas Are Rising

Asia-Pacific holds the largest global market share at 38.64% in 2025, driven by:

- China and India's massive coal extraction volumes

- Australian iron ore operations integrating low-rolling-resistance belts to meet net-zero targets

- Indonesian coal and nickel mining expansion

North America represents a mature but modernizing market. Key regional profiles:

- Western U.S. (Nevada, Arizona): Copper and precious metals drive demand for heavy-duty steel cord belts

- Appalachia: Coal operations prioritize replacement cycles as aging systems retire

- Federal investment: The Inflation Reduction Act allocates billions for domestic critical mineral production, creating downstream demand for material handling systems

While North America's market matures, Latin America is outpacing every other region in growth. Key drivers include:

- Chile's mining investment pipeline for 2024–2033 totals $83.18 billion, split 80% brownfield and 18% greenfield expansions

- Peru, Brazil, Colombia, and Argentina advancing major copper, lithium, and iron ore projects

- Regional conveyor belt demand projected at 6.60% CAGR through 2031 — the fastest of any global region

Technology Trends Reshaping the Conveyor Belt Market

IoT Sensors and Predictive Maintenance

Mining downtime costs can exceed $1 million per day at large operations. IoT-enabled conveyor systems address this directly — embedded sensors and RFID chips monitor:

- Belt wear and steel cord integrity

- Splice degradation and load anomalies

- Real-time fault detection before catastrophic failure

Systems like ContiTech's Conti+ and MultiProtect enable scheduled maintenance windows, extending belt life by 15–20%.

Gearless Conveyor Drives (GCD)

Traditional gearbox-driven systems require frequent maintenance and limit single-flight conveyor lengths. Gearless Conveyor Drives reduce energy consumption by 6–10% and cut CO2 emissions by 6–10%. ABB's 20-MW gearless system at Codelco's Chuquicamata underground mine delivers 11,000 tons per hour on a single flight, trimming vibration by 30% and eliminating gearbox maintenance entirely.

Sustainability Innovations

Energy efficiency gains from GCDs have pushed manufacturers to pursue sustainability across the full belt system. ESG compliance requirements are driving eco-friendlier belt designs across the board:

- Reduce indentation energy loss through low-rolling-resistance (LRR) compounds, cutting electricity consumption by 20–32%

- Use recyclable rubber compounds and bio-based materials to reduce landfill impact at end-of-life

- Lower power draw per ton-kilometer with lighter, high-tensile belt constructions that match the strength of heavier alternatives

Mining operators facing investor scrutiny and tightening emissions regulations increasingly specify these designs at the procurement stage.

Competitive Landscape and Key Players

The mining conveyor belt market is moderately consolidated, with top suppliers capturing approximately 45% of global sales. Key players include:

- ContiTech (Continental AG): Expanded Conti+ digital platform; Continental plans to spin off ContiTech in 2026

- Fenner Conveyors (Michelin Group): Launched OptimaHeat Xtreme high-temperature belts; rebranded to emphasize Michelin ownership

- Phoenix Conveyor Belt Systems (Continental AG): Showcased Phoenocord steel-reinforced belts at MINExpo 2024

- Zhejiang Double Arrow: Strategic partnership with Almex Group; recognized as "Significant Contribution Supplier" by Codelco in 2024

- Yokohama Rubber: Introduced fire-resistant belts for underground mining in 2025

- Bando Chemical: Continues supplying Rock Belt and Monoply Belt impact-resistant lines

Bridgestone withdrew completely from the conveyor belt business by the end of 2024, citing inability to secure long-term profitability. This exit leaves a real gap at the Tier-1 level — operators who relied on Bridgestone now need to qualify replacements before their next procurement cycle.

What this means for buyers: Identify which remaining suppliers cover your specific belt specifications (steel-cord, fire-resistant, high-temperature) and confirm their regional distribution capacity before contracts renew.

What This Market Growth Means for Mining Operations in the Americas

For mining companies across North and South America, market growth translates into operational reality: deeper mines, stricter regulations, and the critical minerals boom all demand conveyor systems that are more durable, more intelligent, and more efficiently sourced.

Key operational imperatives:

- Transition economics: Operators evaluating IPCC systems can model 80%+ operating cost savings versus truck haulage

- Underground expansion: As surface reserves deplete, underground requirements grow—fire resistance, sensor integration, and gearless drives are no longer optional

- ESG compliance: Investors and regulators demand emissions reductions; belt conveyors deliver 70–90% energy and emissions cuts versus trucks

- Supply chain resilience: Bridgestone's exit and Continental's ContiTech spin-off create real supply uncertainty—securing long-term agreements with multiple suppliers is now a strategic priority

The right supply partner matters. A distributor who understands the technical requirements—belt tensile strength, fire ratings, splice specifications—and the procurement realities of cross-border operations adds measurable value. Managing customs compliance and timely delivery to remote mine sites is as critical as the equipment itself.

ESG International Suppliers sources conveyor belt equipment alongside the components mining operations depend on—bearings, motors, pumps, hoses, and fittings—from manufacturers built for industrial-grade performance. Serving operations across North and South America, ESG handles procurement logistics, cross-border delivery, and supply chain coordination so mining teams can focus on production, not sourcing.

Frequently Asked Questions

How big is the conveyor belt industry?

The global conveyor belt industry — spanning food processing, logistics, manufacturing, and mining — was valued at approximately $5.1–$5.9 billion in 2022–2024 and is projected to reach $8.1–$8.3 billion by 2032–2033. Mining is the most capital-intensive segment, consistently commanding the largest share of total market value.

What is driving growth in the conveyor belt mining market?

Three factors are driving growth in the mining conveyor belt market:

- Surging demand for critical minerals like lithium and copper, tied to EV and clean energy expansion

- Automation replacing truck haulage in large mines, driven by lower emissions and better economics

- Underground mining expansion as surface reserves deplete, requiring specialized conveyor systems for confined environments

What types of conveyor belts are most commonly used in mining?

Steel cord belts dominate heavy-duty and deep underground applications due to their high tensile strength and minimal elongation. Textile-reinforced (fabric) belts handle lighter-duty surface work where flexibility and cost efficiency matter most. Aramid and hybrid belts are a growing niche for underground declines and energy-efficient overland routes.

Which region dominates the mining conveyor belt market?

Asia-Pacific holds the largest global share (38.64% in 2025), driven by China's coal operations, India's coal and minerals extraction, and Australia's iron ore majors. North America is a significant mature market focused on modernization, while Latin America represents the fastest-growing region (6.60% CAGR through 2031) due to massive copper and lithium mining investments.

What are the biggest challenges for conveyor belt systems in mining operations?

Mining conveyor systems face three recurring challenges:

- High abrasion and impact from heavy ore loads, causing accelerated belt wear

- Maintenance complexity in underground and remote environments where access is limited

- Significant capital costs for installation and replacement, making commodity price cycles a key budget factor

How is technology changing mining conveyor belt systems?

Three technologies are reshaping mining conveyor systems:

- IoT monitoring and AI-based predictive maintenance detect belt wear before failures cause shutdowns

- Gearless conveyor drives eliminate gearboxes, cutting energy consumption by 6–10% and reducing maintenance needs

- Low-rolling-resistance belt compounds reduce electricity consumption by 20–32%, supporting sustainability and emissions targets